European Commission Is Exploring Options for Introducing New Taxes

The Commission is examining wealth taxes, including inheritance and gift taxes, as well as exit taxes.

Commissioned by the European Commission’s Directorate-General for Taxation and Customs Union (DG TAXUD), a study titled “Wealth Taxation, Including Net Wealth, Capital and Exit Taxes” has been completed. The study examines five types of wealth taxes and considers inheritance, gift, and exit taxes to be the most promising among them. The study was prompted by concerns over wealth distribution, the decline of wealth taxes and taxes on asset transfers in recent decades, and the budget deficits many European countries face due to successive crises.

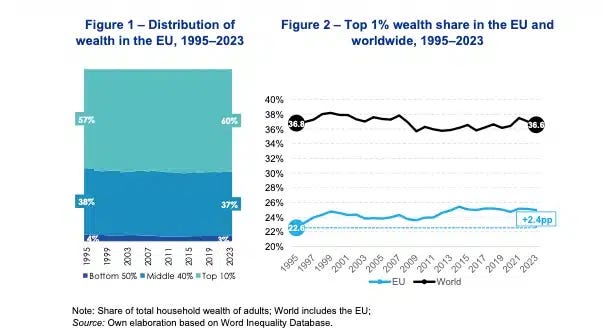

The study notes that over the past thirty years, private wealth in the European Union (EU) has grown significantly, but it has become increasingly concentrated in the hands of the wealthiest households. The share of wealth held by the top 10% has increased in particular. This trend is evident in nearly all EU member states, with the top 1% consistently increasing its share of total wealth – and doing so at a faster rate than its counterparts elsewhere in the world. According to the study, this wealth growth has been driven by rising asset prices and the expansion of pensions and financial portfolios. As a result, the share of the wealthiest is growing in the EU, while wealth growth among middle-class households has been slower. Even the wealthiest 0.01% have seen their wealth increase at a slightly slower rate than their counterparts in some of the countries outside the EU.

The study notes that the concentration of wealth is fast becoming a structural feature of the European economy, yet it remains unclear whether existing taxes are capable of ensuring fairness. Therefore, the study examined five categories of wealth-related taxes: net wealth taxes, recurrent (unrealised) capital gains taxes, non-recurrent (realised) capital gains taxes, inheritance and gift taxes, and exit taxes. It then analysed whether these taxes would help distribute the tax burden more fairly without negatively impacting investment, entrepreneurship, and economic growth.

Rationale for Inheritance and Gift Taxes: Europeans Have a Lot To Pass on

Of all wealth taxes, inheritance and gift taxes most directly target the transfer of assets between generations. According to the study, the macroeconomic significance of inheritances has grown in recent decades. The share of inheritances in government revenue and private wealth has increased in several European countries, and substantial inheritances play an increasingly important role in the formation of a very high net worth – including the creation of billionaires. However, inheritances are highly concentrated, and already wealthy households inherit more frequently and in greater amounts. Thus, according to the study, there is every reason to tax inheritances and gifts, as they are effective tools for increasing revenue and reducing wealth inequality.

Most of the EU countries (17) levy an inheritance tax, but many have abolished it, and some have never introduced it. In countries that still levy an inheritance tax, it is usually progressive. In such cases, tax rates vary based on the relationship between the donor and the recipient; for example, there are tax breaks for spouses and direct descendants, while higher tax rates apply to more distant relatives and non-relatives. In particular, numerous exemptions, concessions, and other preferential treatments apply to business assets and owner-occupied housing. However, all such benefits and special provisions significantly reduce state revenue.

In the case of inheritance and gift taxes, behavioral responses, i.e. how people respond to and cope with them, play a central role. Currently, data on these responses inside the EU remains limited, but it points to a strong motivation to avoid the tax through various means, particularly among wealthy families. These strategies include transferring assets during one’s lifetime (gifts), using other legal measures or tax incentives, and in some cases, moving assets to offshore jurisdictions. However, according to the study, this avoidance behaviour has a rather small impact on entrepreneurship and labour supply, as well as on overall wealth accumulation.

Thus the study concludes that if inheritance and gift taxes are well-designed, feature a broad tax base, integrate gifts and inheritances, are strictly enforced, and offer few opportunities for tax avoidance, then these taxes can effectively contribute to the state budget. At the same time, such taxes would reduce inequality in wealth and opportunity without significant distortion to the economy. In any case, the importance of inheritance and gift taxes will grow even further in the future, as a so-called “great transfer of wealth” from the older generation to the younger one still lies ahead.

Exit Taxes: Country of Origin Should Receive Its Fair Share When People Move Abroad

Exit taxes apply to unrealised capital gains that arise when a person moves or transfers assets abroad. The purpose of the tax is to protect the state’s tax revenue so that profits generated within the country cannot be taken out without being taxed. Currently, EU countries apply exit taxes to different asset types, with varying thresholds, and deferral options. However, under EU law, exit taxes must not unduly hinder the free movement of people, and therefore taxpayers are permitted to pay the tax in installments or on a deferred basis.

The study notes that there is little evidence regarding the behavioral responses to an exit tax. At the sam time, studies on mobility suggest that it is rather rare for the wealthy to move elsewhere. Furthermore, an exit tax is not the main factor that would cause the wealthy to relocate. For them, incentives in the destination country are far more important than taxes. Thus, the study finds that an exit tax can generate revenue even if very few taxpayers are affected. The key is that the tax is simple, clear, with enforceable assessment rules, and benefits from strong international cooperation.

Net Wealth Taxes Work Best When They Target Only the Very Wealthy

According to the study, net wealth taxes are important but rare in Europe. Only a few EU countries currently tax net wealth, such as Switzerland and Spain. However, quite a few countries have abolished their former net wealth taxes, including Germany and Sweden, where a narrow and inconsistent tax base, extensive tax exemptions, the ability to self-assess, and similar factors reduced revenue while creating a sense of unfairness.

The study concludes that a net wealth tax works best when it taxes only the very wealthy, using high thresholds and uniform tax bases and valuation rules. Successful systems depend on reliable asset data, continuous valuation, and the ability to combat tax evasion, such as through debt restructuring or shifting assets into preferential categories. According to the study, key components of a net wealth tax include comprehensive asset registries, third-party reporting, digitalization, and strong enforcement.

At the same time, the study confirms the existence of behavioral responses as such, particularly among the high-net-worth individuals, but these are likely to remain moderate if the tax is well-targeted. Thus a broad-based, uniform, high-threshold, and vigorously enforced net wealth tax could improve revenue. The key is that the tax should not be fragmented or based on distortive incentives.